How Canadian Mortgage Rates Are Likely to be Impacted By the U.S. Fed’s Dovish Shift

February 4, 2019Bank of Canada Governor Poloz May Want Higher Rates, But He Needs Stable Inflation

February 25, 2019 Last Friday, Statistics Canada released our latest employment data, for January, and it showed that our economy added an estimated 66,800 new jobs last month.

Last Friday, Statistics Canada released our latest employment data, for January, and it showed that our economy added an estimated 66,800 new jobs last month.

Interestingly, even though the headline result came in much higher than the consensus estimate of 8,000, the bond market essentially shrugged off the news. I think that is in part because the underlying data weren’t actually that strong, but also because bond market investors don’t believe that last month’s surprising job-growth headline is likely to move the needle much at the Bank of Canada (BoC).

Before we look at the key details from the latest employment data, let’s first circle back to a recent speech made by Deputy BoC Governor Carolyn Wilkins on January 31, 2019 titled “A Look Under the Hood of Canada’s Job Market”. The speech provides a very recent BoC assessment of the health of our overall job market, and it provides insightful context for evaluating last month’s employment data.

Here are the highlights from Deputy Governor Wilkins’ speech:

- Wilkins explained that “the job market is a bellwether of financial health and a useful gauge of inflation pressures” for the BoC and assessed that the job market “is in good shape”. She also noted that “firms across the country tell us that it’s difficult to fill openings”.

- That said, Wilkins noted that “wages overall in Canada are not rising as fast as we would expect given how low unemployment is”. The Bank believes that subdued wage growth may be a signal that “the job market may have more room to run.” If that proves true, inflationary pressures will take longer to build, and there will be less urgency for the Bank to raise its policy rate.

- The BoC estimates that when our economy reaches full employment, which will be the point when incremental labour demand pushes wage costs and overall inflation materially higher, we should see “wage growth of around 3 per cent”.

- Our overall wage growth is being skewed by subdued wage growth in our energy-intensive regions, which “continue to lag behind those in the rest of the country”. The current wage-growth gap between our energy-intensive regions and our non-energy-intensive regions is about .75%. (The BoC estimated that in the third quarter of 2018, wage growth in our energy-intensive regions averaged just under 2%, while it came in at about 2.75% in Ontario and Quebec.)

- The BoC believes that our current period of slower-than-expected wage growth is also explained, in part, by recent domestic trends. These include skills mismatches between employees and job requirements that affect about “1 out of every 10 jobs in Canada”, and lower job turnover rates (which the BoC refers to as “churn”) that are being caused by a combination of factors. These include more cautious employees, housing affordability constraints, and uncertainty about commute times and jobs prospects for partners and spouses in alternative locations.

- The Bank also attributes our weak wage growth to structural factors that “are being felt in many advanced economies”. (As a reminder, structural factors are unaffected by changes in the BoC’s monetary policy.) These include technological advances, increased global competition, and the rise of “superstar firms” that kill off competition, and in the process, limit employment alternatives for workers (which lessens their bargaining power). At the same time, the ongoing rise in short-term contract work and in “non-standard jobs” has created more marginally employed workers who are typically paid less and who have very limited job stability.

Now let’s look at the highlights from our January employment data, while keeping Deputy Governor Wilkins’ observations in mind:

- Our service-producing industries added 99,000 new jobs last month but our goods-producing industries lost 32,000 jobs in January. We haven’t seen any expansion in goods-producing employment over the last twelve months against a backdrop of heightened trade uncertainty. That’s cause for concern because these jobs create a multiplier effect for employment growth across our broader economy.

- Private-sector employment increased by 112,000 jobs, public sector employment was unchanged, and the number of self-employed workers fell by 61,000 jobs. The surge in private-sector employment marked the biggest month-over-month increase since Stats Can started tracking these categories in 1976.

- Ontario (+41,000 jobs) and Quebec (+16,000 jobs) led the way last month, while Alberta experienced the biggest decline (-16,000 jobs). In addition to fuelling the wage-growth gap between these provinces, the negative economic impacts from job losses in our energy-sector region are being exacerbated by the skills mismatches and lower job turnover rates that BoC Deputy Governor Wilkins outlined in her speech.

- Our unemployment rate rose from 5.6% to 5.8% but only because more disenfranchised Canadian workers came off the sidelines. On that note, the participation rate, which measures the percentage of working-age Canadians who are either working or actively looking for work, rose from 65.4% to 65.6%.

- Of the new jobs created last month, 52,800 were for workers aged 15 to 24. That will come as a relief to BoC Governor Poloz, who recently said that the current lack of employment opportunities for our youth is what keeps him up at night. (The unemployment rate for this age group now stands at 11.2%.) Meanwhile, there was virtually no employment growth in January for workers aged 25 to 54, which has been the case for essentially the past twelve months. (This key age group is otherwise known as the “breadwinner category” because it is associated with the highest average incomes levels.)

- Average wage growth for permanent employees increased by 1.8% on a year-over-year basis in January. While that tally was up from 1.5% in December, it was still well below the peak of 3.9% we saw last May. Perhaps even more importantly, it still hovers below our overall inflation rate of 2% which means the purchasing power of the average permanent worker is still contracting. That trend does not portend well for consumer spending, which is a key source of growth for our economy. (Canadian consumers account for about 58% of our overall GDP.)

- That said, the BoC also generates a different, more detailed measure of wage growth called “wage-common” which paints a more encouraging picture. Wage-common has averaged 2% over the past five years and it picked up to 2.3% in Q3 2018. That is closer to the 3% threshold that the BoC will use as a signal that our economy has reached full employment, but with ample room still to spare.

- Average hours worked rose by 1.2% on a year-over-year basis, but fell by 0.3% month-over-month. Economist David Rosenberg estimates that this reduction is equivalent to a decline of 128,000 in January (which is more than double our headline jobs gain).

When we look beyond last month’s employment headline, the data offer more of a mixed bag of results.

Job growth is strong in the service sector, but not in our long beleaguered and critically important goods-producing sector. Our non-energy intensive regions are generating employment opportunities but our energy-intensive regions are still struggling. We see a surge in youth employment, but stagnant growth in the key breadwinner category. Wage growth remains lower than expected in part because of structural changes across most advanced economies, but also because of Canada-specific factors such as skills mismatches and low turnover rates that are making our labour force less resilient and responsive.

Against that backdrop, the bond market essentially treated last month’s employment data with a yawn.

That’s not altogether surprising because as BoC Deputy Governor Wilkins reminded us at the end of her recent speech, in the current environment the Bank’s primary focus is on “how oil prices, the Canadian housing market and global trade policy evolve.”

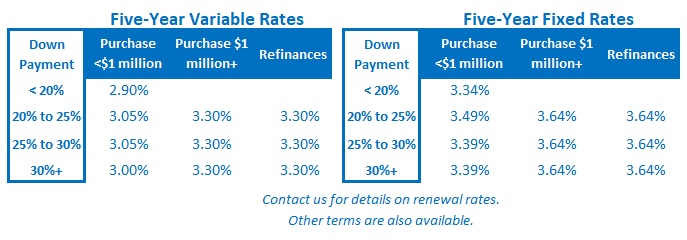

The Bottom Line: Last week’s banner Canadian employment headline had very little impact on Government of Canada bond yields in part because the underlying data showed mixed results, as outlined above, and also because the BoC is focused on other key areas of our economy at the moment. That explains why the latest jobs release had little impact on either our fixed or variable mortgage rates.

The Bottom Line: Last week’s banner Canadian employment headline had very little impact on Government of Canada bond yields in part because the underlying data showed mixed results, as outlined above, and also because the BoC is focused on other key areas of our economy at the moment. That explains why the latest jobs release had little impact on either our fixed or variable mortgage rates.