A Review of Our Latest Employment Report with Implications for Canadian Mortgage Rates

May 13, 2013Out With the Old Bias, In With the New Bias?

May 27, 2013 Anyone keeping an eye on Canadian mortgage rates should pay close attention to the Consumer Price Index (CPI) which is released monthly by Statistics Canada. The CPI tells us whether average prices have increased or decreased over the past twelve months, and over time, changes in the CPI influence Bank of Canada (BoC) monetary policy more than any other economic measurement.

Anyone keeping an eye on Canadian mortgage rates should pay close attention to the Consumer Price Index (CPI) which is released monthly by Statistics Canada. The CPI tells us whether average prices have increased or decreased over the past twelve months, and over time, changes in the CPI influence Bank of Canada (BoC) monetary policy more than any other economic measurement.

Before looking at the details in the latest CPI (released last Friday), let’s highlight a few phrases from the BoC’s oft repeated inflation-control strategy, which it includes at the front of each Monetary Policy Report (MPR).

- At the heart of its inflation-control strategy, the BoC believes that “that the best way to foster confidence in the value of money and to contribute to sustained economic growth, employment gains and improved living standards is by keeping inflation low, stable and predictable”.

- Further to that point, the BoC’s inflation-targeting approach is symmetric, meaning “that the Bank is equally concerned about inflation rising above or falling below the 2 per cent target”.

As you will see in a moment, that last phrase is critical in the current context. If the BoC’s monetary policy actions are primarily governed by the goal of steering inflation towards 2% over time, then current CPI trends clearly imply that the BoC’s next move in its overnight rate should be a decrease, rather than the increase it has repeatedly warned us about.

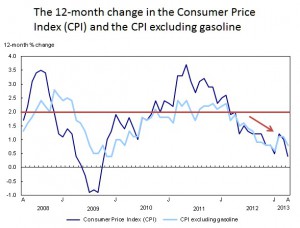

The latest CPI data show that average prices rose by a paltry 0.4% over the most recent twelve months ending in April (down from 1% in March). The largest contributor to this drop was falling gas prices but even with the change in gas prices stripped out, overall CPI would still only have risen by 0.8% – a far cry from the BoC’s 2% target. As the chart by Stats Can on the right shows, our CPI has now been below the BoC’s target rate of 2% for over a year and much of our supporting economic data, such as GDP growth and unemployment rates, are more consistent with continued disinflation and even deflation, not inflation.

right shows, our CPI has now been below the BoC’s target rate of 2% for over a year and much of our supporting economic data, such as GDP growth and unemployment rates, are more consistent with continued disinflation and even deflation, not inflation.

In its most recent MPR the Bank of Canada forecasted that inflation would return to its 2% target in mid-2015 but as with so many of the BoC’s predictions of late, that one is also now ripe for some downward revision. In fact, we seem so far away from returning to that target rate that I think it’s time to suggest that the BoC may need to give us a little help to get back there.

As unlikely as it may sound to Canadians who have grown accustomed to former BoC Governor Carney’s warnings about imminent rate increases, at some point the BoC may have no choice but to lower its overnight rate. Our economy is dangerously close to stall speed and if you want a look at just how far central bankers are willing to go to stave off the threat of deflation and/or recession, look no further than U.S. Fed Chairman Ben Bernanke and his ever-whirring printing presses. A little drop in our overnight rate hardly seems radical by comparison.

The BoC’s main reason for not dropping rates has long been our record household debt levels, which it has called “the biggest threat to our domestic economy”. But the increase in our household borrowing rates has slowed dramatically of late and as strange is it may sound, there may come a day when lowering rates in an attempt to stimulate a little more household borrowing will seem like a price worth paying if it keeps our economy afloat.

To be clear, I don’t believe that a rate cut is imminent and my best guess is that rates aren’t likely to go up or down significantly for the foreseeable future. In fact, even if the data continue to indicate that the BoC should cut its overnight rate, the Bank may still question whether a marginal decrease would have any material impact on consumer spending in our already well-entrenched, ultra-low rate environment. But if we’re going by the BoC’s official inflation-control strategy, I think the recent data continue to lend support to the rate-decrease option.

Government of Canada (GoC) five-year bond yields were two basis points higher for the week, closing at 1.36% on Friday. Not all lenders have raised rates in response to the recent bond-yield run up and as such, five-year fixed rates are still available in the sub-3% range.

Five-year variable-rate mortgages are available in the prime minus 0.45% range, which works out to 2.55% using today’s prime rate.

The Bottom Line: The latest CPI from Statistics Canada shows that average prices have barely risen over the most recent twelve months. These data bolster my long-held belief that fixed- and variable-mortgage rates aren’t likely to rise for the foreseeable future and lends support to the argument, at least in theory, that the BoC’s next change to its overnight rate is still most likely to be a decrease.