U.S. Fed Chairman Bernanke Talks Bond Yields Down. Will Mortgage Rates Follow?

July 15, 2013Why the U.S. Fed’s Most Recent Commments Are Good News for Canadian Mortgage Rates

August 6, 2013 The Bank of Canada (BoC) met last week and decided to keep its overnight rate unchanged, as expected.

The Bank of Canada (BoC) met last week and decided to keep its overnight rate unchanged, as expected.

The BoC also issued its latest Monetary Policy Report (MPR) which I read with great interest because it gives us the Bank’s views on the state of the world’s economies and includes projections on where the BoC sees both foreign and domestic economies headed over the next several years.

In the latest MPR, the BoC forecasted that the Canadian economy would return to full capacity sometime in mid-2015. Not surprisingly, this mirrors the consensus forecast of when the U.S. economy is expected to reach full capacity – although both estimates are dependent on rather optimistic assumptions.

When an economy reaches full capacity, inflationary pressures increase and that’s why expectations of when the BoC will next increase its overnight rate converge around the mid-2015 time frame. (As a reminder, Canadian variable-rate mortgages are priced using the BoC’s overnight rate.)

That got me thinking. Since there is now a fairly widespread view that the BoC and the U.S. Federal Reserve won’t start increasing short-term rates until mid-2015 at the earliest, how high would variable rates have to rise after mid-2015 before borrowers who took a variable-rate mortgage today would end up with about the same overall borrowing cost as those who opted for a five-year fixed-rate mortgage instead?

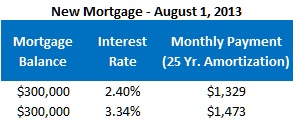

To answer this question, let’s start by assuming that you take out a mortgage of $300,000 on August 1, 2013 and that you are currently choosing between a five-year variable rate at 2.40% (prime minus 0.60%) and a five-year fixed rate at 3.34%.

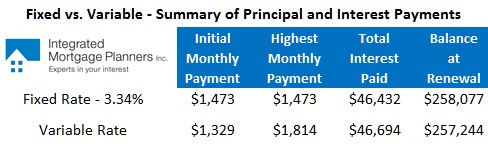

For the reasons outlined above, we’ll assume that the first variable-rate increase of 0.25% will occur on August 1, 2015. From that point on, we assume that the BoC increases its overnight rate by 0.25% every three months over the remaining three years, which means that your variable rate would rise to 5.40% by the end of your five-year term.

This scenario translates into twelve 0.25% rate increases over thirty-six months. To put that in perspective, this aggressive tightening of monetary policy would greatly exceed the magnitude of the last five tightening cycles that have been implemented by the BoC over the past fifteen years (and that’s as far back as I checked).

Here is a comparison of how five-year fixed- and variable-rate borrowers would fare under this scenario:

Let’s add one more wrinkle to this comparison.

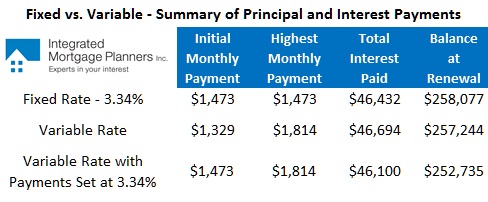

I regularly advise my variable-rate mortgage borrowers to bank the savings inherent in today’s variable-rate mortgage by setting their monthly payment as if they had actually taken a five-year fixed rate of 3.34% instead. In this case, that would mean increasing the monthly payment from $1,329 to $1,473, which we would do by calling the lender and asking them to take an ongoing additional, discretionary payment of $143 every time the regular monthly payment of $1,329 is taken. (The lender can put a note on file so that this extra amount is taken automatically for as long as you leave the instruction in place, meaning that you don’t have to call every month to keep this arrangement going).

I love this strategy because it gets you used to paying a higher rate (3.34% instead of 2.40%) and as such, if your variable rate rises, you simply adjust the $143 discretionary payment down so that your total monthly payment remains at $1,473 until your variable rate rises above 3.34%. In the meantime, you pay off your mortgage more quickly and increase the odds that you will have a lower mortgage balance at renewal, even if your rate rises precipitously in the latter part of your term.

Here is the comparison chart again with the results from this make-hay-while-the-sun-shines approach for variable-rate borrowers included:

Surprised? The key to this scenario is the assumption that the variable rate doesn’t begin to move until mid-2015. If the BoC doesn’t move its overnight rate until then, as you can see in the example above, even frequent and consistent rate increases over the remaining three years of the term are manageable.

Five-year Government of Canada bond yields dropped another nine basis points last week, closing at 1.66% on Friday. Despite a twenty-one basis-point drop in yields over the past two weeks, lenders have not yet lowered their five-year fixed rates in response. Some have speculated that this is because lenders used the previous round of fixed-mortgage rate increases to pass on higher back-end funding costs to consumers. While this explanation may be accurate, I expect natural market forces to rekindle more aggressive rate competition soon enough.

Five-year variable-rate mortgages can still be found with discounts of as much as prime minus 0.60% (which works out to 2.40% using today’s prime rate). If you’re considering a variable rate, check out my post on how different lenders apply interest-rate compounding to their variable-rate mortgages. This is a fine-print detail that is overlooked by most borrowers.

The Bottom Line: Recent comments by the BoC and the U.S. Fed suggest that neither Canadian nor U.S. short-term policy rates are expected to go anywhere until at least mid-2015. If that’s true, as the calculations in today’s post show, the odds that a variable-rate mortgage will save you money over the next five years are stacked in your favour.