Fixed Rates Move Up and Variable Rates Look Better By Comparison

June 17, 2013Why the Variable-Rate Mortgage is Looking Better All the Time

July 8, 2013 Last week borrowers saw five-year fixed-mortgage rates rise, and then rise again, ending the era of sub-3% five-year fixed rates … at least for the time being.

Last week borrowers saw five-year fixed-mortgage rates rise, and then rise again, ending the era of sub-3% five-year fixed rates … at least for the time being.

Lenders raised their rates in reaction to surging Government of Canada (GoC) five-year bond yields, which have now increased by 66 basis points over the last seven weeks.

As a first step toward understanding what all this means for our mortgage rates over the short and medium term, let’s start by taking a look at how we got to this point.

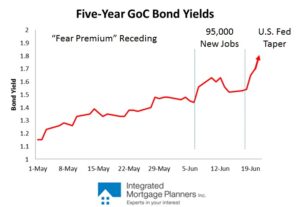

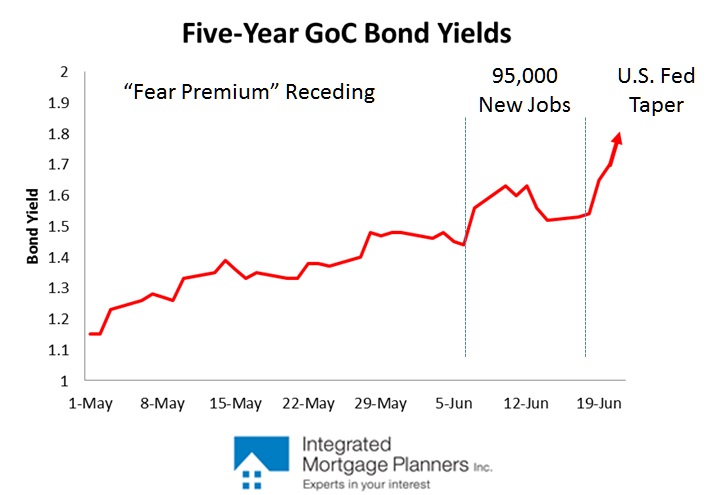

The run-up in five-year GoC bond yields has occurred in three distinct phases which were fueled by separate but mutually reinforcing factors:

- A reduction in the “fear premium” that investors were willing to pay for the safety of GoC bonds. During this phase, from May 1, 2013 to June 6, 2013, the GoC five-year bond yield rose from 1.15% to 1.44%. In a post, written three weeks ago, I predicted that renewed fears of tail-risk events, like more euro-zone instability and/or a Japanese bond-market shock, would eventually re-inflate this premium.

- A near-record spike in the Canadian employment data showed 95,000 new jobs created in the month of May. This report was released by Statistics Canada on June 7, 2013 and bond yields surged 19 basis points over the next two trading days. In a post, written two weeks ago, I predicted that any impact from our May employment report would be minimal and highlighted several concerns with the details in the report that were obscured by the banner headline. Interestingly, bond yields fell back 9 basis points and were in retreat until …

- An announcement last Wednesday by the U.S. Federal Reserve that later this year it would begin tapering its massive $85 billion per month program to purchase U.S. treasuries and mortgage-backed securities. The Fed also outlined a more optimistic economic forecast in support of this plan.

While the first two factors weren’t enough to change my long-held view that five-year fixed rates would not materially rise for the foreseeable future, the U.S. Fed’s latest announcement is a potential game changer. We live in strange times where the role of central banks has shifted from influencing markets with an invisible hand to being an active, direct and leading, market participant. As such, when the Fed softens its open-ended commitment to be the marginal, and largest, buyer of U.S. Treasuries, you can bet that U.S. Treasury yields will rise in the aftermath. Against this back drop, higher Canadian fixed-mortgage rates are inevitable because GoC bond yields have had a 98% correlation with U.S. Treasury yields over the past five years (thanks to BMO economist Doug Porter for that statistic).

But will the U.S. Fed follow through and taper its quantitative easing programs within the timetable it now prescribes? The Fed carefully qualified its schedule with caveats about the economy, jobs, and (implicitly) equity markets, performing as expected. As such, if equity markets continue to weaken, and/or business investment and employment growth slow, these developments could easily cause the Fed to delay its tapering plans. This is a very realistic possibility. The experts I read have long said that starting quantitative easing (QE) is as easy as squeezing toothpaste from a tube and ending it is about as complicated as trying to put that toothpaste back again (and we’re talking about the multi-coloured kind of toothpaste in this analogy).

The Fed’s QE programs have created massive market distortions that won’t right themselves without sending shock waves through an economy that is still on a fragile footing. Consider the following:

- The U.S. Fed is counting on the continued recovery of the U.S. housing market but the rise their latest comments have triggered in Treasury yields has already pushed U.S. mortgage rates 0.50% higher, before any actual QE tapering has even begun. The U.S. housing recovery has thus far been primarily fueled by well-heeled private and corporate investors, not the all-important first-time buyers whose increased participation will be critical to any sustainable momentum in the housing market. First-time buyers are highly sensitive to these now rising mortgage-borrowing costs, especially since many of them are already awash in record levels of student debt. If the Fed’s tapering plans push Treasury yields significantly higher, this will create a powerful headwind for the U.S housing recovery.

- Average price-to-earnings (P/E) ratios for equities are above their long-term averages and this latest bull-market run has recently had much more to do with the Fed’s ultra-loose monetary policy distorting prices than with actual improvements in corporate earnings. If equity markets continue to decline as the Fed begins to taper, this will undo the wealth effect that the Fed worked so hard to create in the first place and could easily force the Fed to slow the timing of its QE withdrawal.

- The Fed revised its 2013 GDP growth forecasts for the U.S. economy down into the 2.3% to 2.6% range, but now calls for U.S. GDP growth to rebound to 3.25% in 2014, based largely on a recovery in export demand. Given the fragile state of the world economy, this forecast is far from assured. (Side note: I’ve noticed that central banks have a habit of raising their medium-term forecasts when lowering their short-term forecasts, only to then revise them gradually back down as they move closer to the present. The Fed appears to be following this well-worn playbook and as such, I am instinctively skeptical about the upward revision to its 2014 GDP growth forecast which got the markets so riled up last week. Interestingly the IMF reduced its forecast for U.S. GDP growth in 2014 from 3% to 2.7% last Friday.)

- Before they became modern-day rock stars who determine market winners and losers, central bankers were charged with the boring old task of keeping inflation stable. The U.S. Fed’s target for inflation is 2.5% but it came in at 1.4% in May and in its latest commentary, the Fed acknowledged that inflation might drop below 1% this year. In Canada, our target inflation rate is 2%, and last Friday Statistics Canada confirmed that our latest Consumer Price Index (CPI) for May came in at a meager 0.7%, up from 0.4% in April. Both inflation rates are well under target and this implies the need for looser, not tighter monetary policy.

Although we ignore the Fed’s warnings at our peril, I can’t help wondering whether the Fed’s change in tone was really just a trial balloon to see how the market will react when the day of reckoning, or in this case, the day of tapering, actually arrives. The Fed certainly left itself plenty of room to alter its timing if circumstances warrant. In the words of Ben Bernanke: “Our policies are going to depend on this [improved] scenario coming true. If it doesn’t come true, we’ll adjust our policies.”

In the meantime, investors will carefully inspect every piece of new data with a fine tooth comb in an attempt to pinpoint when the Fed will actually begin to taper. This guessing game should incite more volatility in bond yields, and markets in general, in the months to come.

Five-year GoC bond yields were up 29 basis points last week, closing at 1.81% on Friday. Five-year fixed rates are now offered in the 3.25% range while ten-year fixed rates are still available in the 3.64% range. If you value the stability of fixed rates and believe in the strength and sustainability of the U.S. recovery, paying a small premium (0.40%) to lock-in a rate for an additional five years of protection seems like an easy call. If rates start to rise in a major way, the second five years could be a lot more important than the first five. (Most people don’t know that breaking a ten-year fixed-rate mortgage after the fifth year only costs you a penalty of three months’ interest. For more details, here is my post on the ten-year fixed rate, which I took many years ago as my first mortgage.)

Five-year variable-rate mortgages are available in the prime minus 0.50% range (which works out to 2.50% using today’s prime rate). Even if the Fed’s tapering plans come off without any major hitches the removal of its QE programs will still provide a headwind for the U.S. economy. This should push out the timing of any change to the Fed’s policy rate, and by close association, the Bank of Canada’s overnight rate (on which our variable rates are based). In fact, at their latest meeting, fifteen of the nineteen members who sit on the committee that sets the U.S. Fed’s policy rate forecasted that it would not be increased until 2015 or later.

The Bottom Line: We are now at an inflection point with mortgage rates and there are two evolving views of where we are headed. If you believe that the U.S Fed QE taper will not cause serious damage to the U.S. economy, with five and ten-year fixed rates so closely aligned, I think the ten-year fixed rate is worth the 0.40% premium you pay for the five extra years of rate certainty. If you believe that volatility and fear will remain the watchwords of central bankers and investors for the foreseeable future, then I think the five-year variable rate is a far more compelling option than the five-year fixed rate, especially given the 0.75% gap that now exists between them.