Canada’s Vibecession No More

June 1, 2026

The Bank of Canada’s Balancing Act

June 15, 2026

Last week Statistics Canada confirmed that our economy added 88,000 new jobs in May, well above the 10,000 expected by the consensus.

Last week Statistics Canada confirmed that our economy added 88,000 new jobs in May, well above the 10,000 expected by the consensus.

The stronger-than-expected employment report was a welcome reprieve from our recent string of downbeat economic releases. The banner headline was supported by solid underlying details.

Our unemployment rate declined from 6.9% in April to 6.6% in May. We added 154,000 new full-time positions, and the private sector expanded by 54,000 new jobs. The gains were also spread broadly across different sectors, including the interest-rate sensitive construction sector (+27,000), and our trade-beleaguered manufacturing sector (+15,000).

Average hourly wages increased by 3.0% (annualized) in April, down from 4.5% (annualized) in May. At that level, average wages are still outpacing overall inflation (2.8% in April) but not to a degree that should raise concerns about cost-push inflation linked to higher energy prices adding pressure to labour costs.

In the broader context, last month’s employment gains only partially recover the losses experienced in other recent months.

With the May gains factored in, our economy has lost a net 5,000 jobs thus far in 2026, and our unemployment rate is a little higher now (6.6%) than it was in January (6.5%).

On balance, our latest employment data offer hope that the summer will bring brighter economic days ahead, as does Stats Can’s initial estimate that our GDP increased by 0.4% in April (month-over-month).

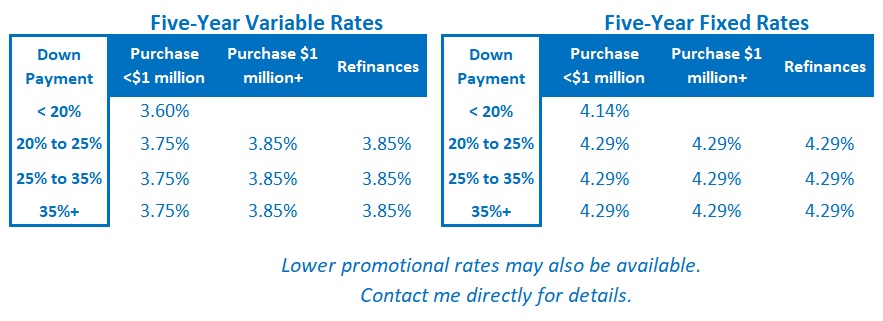

The Latest on Mortgage Rates

Government of Canada bond yields increased a little last week. Most of that rise was likely attributed to the gravitational pull of their US Treasury equivalents.

US Treasuries rose in response to stronger-than-expected US employment data. The US economy has now added 500,000 new jobs thus far in 2026, which is nearly double the 300,000 positions that it added throughout a tough 2025.

US bond-market investors have now completely priced out any rate cuts by the US Federal Reserve this year. Instead, they now expect one 0.25% Fed hike at its final meeting in December.

Canadian mortgage fixed rates held steady last week. So did the current discounts off prime that are being offered on variable mortgage rates.

I expect the Bank of Canada to hold its policy rate steady when it meets this Wednesday. I also expect the Bank to maintain a neutral stance in its accompanying communications, as it balances the upside risks to inflation from spiking energy prices against the downside risks emanating from trade uncertainty.

My Take on Today’s Mortgage Options

My advice is unchanged from last week. Fixed rates are likely to remain volatile.

Three- and five-year fixed rates remain the most popular choices. If the spread between those two options is minimal, I think five-year fixed rates offer better value.

Most of the borrowers I am working with right now are opting for the stability of fixed rates, and I fully appreciate their appeal.

That said, the relative saving offered by today’s variable rates has increased now that spiking bond yields are putting significant near-term pressure on fixed mortgage rates.

I expect that variable mortgage rates will produce the lowest borrowing cost over their full five-year terms, although the potential that they will take borrowers on a bumpy ride has increased since the start of the US/Iran war.

BoC Governor Macklem has confirmed that the Bank will look through the current inflation spike over the near term. But if the war drags on and its associated inflationary impacts become broader and more entrenched, there may come a time when the Bank is compelled to tighten.

For now, my assessment is that we won’t get to that point. But so much depends on how long the US/Iran war will last and if/when the Strait of Hormuz will re-open.

Important note: Anyone choosing a variable rate should do so only if they are comfortable with its inherent potential for volatility. Borrowers must also have the financial capacity to withstand higher costs (and in some cases, higher payments).

Insider’s Tip for Borrowers

This post offers mortgage advice to homeowners who are trying to work through a divorce.

It outlines some key steps that must be taken prior to removing a spouse from title and/or completing a refinancing to buy them out. It also includes several other useful tips that I have accumulated over many years of helping borrowers navigate a marital split.

Three Posts Every New Visitor to My Blog Should Read

This post provides a detailed comparison of the pros and cons of fixed- and variable-rate mortgages amidst trade-related economic uncertainty.

For myriad reasons, some of them unanticipated, many Canadians end up having to break their fixed-rate mortgages. This post provides a detailed breakdown of the very different ways that lenders calculate their fixed-rate mortgage penalties. The amounts charged can vary significantly from lender to lender.

This post provides a detailed summary of the key terms and conditions to pay attention to in your mortgage contract. (They are not standard and can vary in important ways.)