The New Bank of Justin and Bill

March 25, 2019Bank of Canada Governor Poloz Dampens Rate-Cut Speculation

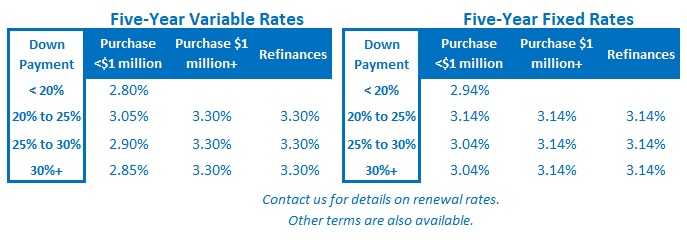

April 8, 2019 Canadian fixed mortgage rates have been on a steady downward march of late.

Canadian fixed mortgage rates have been on a steady downward march of late.

Their decline has been underpinned by softening domestic economic data, which have pushed down Government of Canada (GoC) bond yields, on which our fixed mortgage rates are priced. Our weakening economic backdrop has also made the Bank of Canada (BoC) more dovish about its plans to hike its overnight rate, on which our variable mortgage rates are priced.

While our own slowing economic momentum has been the primary driver of our falling bond yields and mortgage rates, changes in the U.S. Federal Reserve’s outlook are also contributing to their recent drop. That’s because we sell about 80% of our exports into U.S. markets, and on a comparative basis, our provinces trade more with their U.S. neighbours to the south than they do with each other.

Here is a summary of the recent U.S. developments that are helping to put downward pressure on our bond yields, and by association, our mortgage rates:

- The Fed made it clear that it is done hiking rates for the time being. At its policy-rate meeting on March 20, it noted that “growth of economic activity has slowed from its solid rate in the fourth quarter” and that “indicators point to slower growth of housing spending and business investment in the first quarter”. On a related note, last week the U.S. Bureau of Economic Analysis lowered its initial estimate of U.S. fourth quarter annualized GDP growth from 2.6% to 2.2% (which was down from 3.4% in the third quarter).

- At the Fed’s January meeting, the median forecast from its members, who vote on policy-rate changes, was for two rate hikes in 2019. At its latest meeting, that median forecast was revised to no rate increases in 2019 and one increase in 2020.

- U.S. bond-market investors are even more bearish. The U.S. yield curve has now inverted, which means that 3-month U.S. Treasury Bills now offer higher yields than 10-year U.S. Treasuries. An inverted U.S. yield curve is a worrying signal because on a historical basis, a U.S. recession has followed within one year of inversion 85% of the time. (FYI, the Canadian yield curve also inverted recently, but it is not as reliable a predictor of Canadian recessions.) Not surprisingly, the U.S. bond futures market is now betting that the Fed’s next move will be a cut.

- In November 2017 the Fed began to reduce its massive $4.5 trillion balance sheet by allowing $50 billion worth of expiring Treasury securities to roll off its balance sheet each month. This was another form of monetary-policy tightening because it put upward pressure on U.S. Treasury yields as each $50 billion tranche had to be absorbed by the broader bond market. In late 2018, Fed Chair Powell said that this program would continue on auto-pilot, but as U.S. financial conditions tightened sharply shortly thereafter, he quickly backtracked on that statement. At its March 20 meeting, the Fed said that it would slow its monthly balance-sheet reductions to $30 billion in May and stop them altogether by October.

- Fed officials are now talking about a concept called “inflation targeting” which basically means that the Fed would allow inflation to exceed its 2% target after an extended period of below-target inflation in order to ensure that longer-term inflation expectations remained anchored at 2%. If the Fed is willing to allow inflation to run hot, at least temporarily, that further reduces the likelihood of additional Fed rate hikes over the short and medium term.

Interestingly, none of the Fed’s voting members is calling for a rate cut yet. As with the BoC, the Fed prefers to shift its outlook incrementally, over several meetings. Nonetheless, there is no question that its outlook has become decidedly more dovish of late.

So how is this impacting Canadian bond yields and mortgage rates?

The Canadian economy came through the 2008 financial crisis remarkably well, but our growth was largely fuelled by a rise in consumer spending that was underpinned by a massive increase in our overall household-debt levels. Going forward, five recent BoC rate increases and seven rounds of prudent mortgage rule changes make it unlikely that consumer spending will continue to drive our economic momentum.

Instead, the BoC is forecasting/hoping that export growth will fuel a rise in business investment and that these factors will combine to fill the void that slowing consumer spending leaves behind (even though when taken together, they only account for about half of what consumer spending contributes to our overall GDP). For that to have any chance of happening, we need the Loonie to be priced at levels that make our exports competitive. Bluntly put, if the BoC raises rates while the Fed stands pat, or if the Fed starts cutting and the BoC remains on hold, the Loonie would soar higher against the Greenback and intensify an existing headwind that will hammer our exporters.

Against that backdrop, the BoC’s monetary policy needs to track the Fed’s policy closely. Bond market investors know this, and that’s why the Fed’s dovish shift is helping to put downward pressure on our bond yields.

Side note: All that said, last Friday gave us a reminder that macroeconomic trends don’t typically move in a straight line. We learned that Canadian GDP grew by 0.3% on a month-over-month basis in January, which was well above the consensus estimate of 0.1%. That was unequivocally good news, and to be clear, I would trade an economic expansion and higher mortgage rates for slowing economic momentum and lower mortgage rates any day of the week.

What falling bond yields, the BoC, and the Fed are signalling shouldn’t be taken as good news just because it is likely to push mortgage rates lower. In such an instance, cheaper borrowing costs will offer only a silver lining to the dark economic clouds ahead.  The Bottom Line: The U.S. Federal Reserve has sounded much more dovish of late, and that, coupled with reduced economic momentum in Canada, has helped push our bond yields, and by association, our fixed mortgage rates lower. Furthermore, if the Fed is done hiking rates, our export dependence on U.S. markets will ensure that the BoC is done hiking too. That means that our variable mortgage rates, like our fixed rates, aren’t likely to head higher any time soon.

The Bottom Line: The U.S. Federal Reserve has sounded much more dovish of late, and that, coupled with reduced economic momentum in Canada, has helped push our bond yields, and by association, our fixed mortgage rates lower. Furthermore, if the Fed is done hiking rates, our export dependence on U.S. markets will ensure that the BoC is done hiking too. That means that our variable mortgage rates, like our fixed rates, aren’t likely to head higher any time soon.