The Fed’s Imminent Rate Hike May Cause a Surprising Market Reaction

May 2, 2022US Inflation Falls in April (Sort of)

May 16, 2022

Last week we received the April employment data on both sides of the 49th parallel, and the US Federal Reserve made its much-anticipated policy-rate announcement.

Let’s dive right into the details that will be noteworthy for anyone keeping an eye on Canadian mortgage rates.

- The Fed’s Rate Hike

Last week the Fed announced that it would raise its policy rate by 0.50% to a range of 0.75% to 1.00%, marking its largest hike in more than two decades.

The Fed also announced that in June it will begin to sell the Treasuries it purchased from the bond market under its pandemic-related quantitative easing (QE) programs back into that market at a pace of $47.5 billion/month. This provides another form of monetary-policy tightening because that increased supply of Treasuries should lower their prices, causing their yields, and the interest rates that are priced on them, to rise.

In his accompanying press conference. Fed Chair Powell espoused a strategy of “front-end loading” rate hikes to get out in front on the current inflationary pressures. As a result, the bond market is now pricing in additional 0.50% hikes at the Fed’s next three meetings on June 15, July 27, and Sept 21 with a succession of quarter-point hikes to follow thereafter.

The Fed is following a similar approach to that being employed by the Bank of Canada (BoC), which I wrote about recently. It wants to return its policy rate rapidly back to the neutral rate, which is defined as the rate that neither stimulates nor constrains economic growth.

The neutral rate is a theoretical construct that can be difficult to calculate precisely, but the Fed now pegs it at about 2.4%, and that helps explain why financial markets expect the Fed to raise is policy rate by another 1.5% in short order.

The Fed has hinted that once it returns the policy rate to its neutral-rate range, it may pause to allow time to observe the impact of its rapid succession of hikes, which can take a year or more to fully materialize. Last week, Powell acknowledged the risk that this lag effect can have when he said that “if a central bank tightens policy in response to factors that turn out to be temporary, the main policy effects are likely to arrive after the need has passed.”

- Canadian Employment Data

The Canadian economy added 15,300 new jobs last month, well short of the consensus forecast of 40,000. Unfortunately, a closer look at the details reveals that our economy added 47,000 part-time jobs but shed 31,000 full-time jobs.

The biggest losses were in the construction sector (-21,000) and that may be an early sign that the most interest-rate sensitive parts of our economy are starting to feel the effects of sharply higher rates. Next month’s construction numbers will also be impacted by the fact that 15,000 unionized construction workers in Ontario walked off the job last week to lobby for higher pay to compensate for rising inflation.

Our unemployment rate dropped to 5.2%, but total hours worked fell by 1.9% in April and average wages rose by only 3.3% on a year-over-year basis, which is only about half of our current rate of inflation. That means that the purchasing power of the average worker is decreasing – and that wage/price gap is a headwind for consumer spending and overall demand. That said, the minority of workers who do have bargaining power are using it.

The question that continues to confound most employment/wage growth forecasts is Why aren’t wages breaking out if our labour market is now the tightest it has been in nearly fifty years?

I think the answer to that question is that our federal government’s COVID stimulus payments to businesses had the effect of tying employees to their former employers. By subsidizing labour costs, these stimulus payments caused businesses to over-employ based on their actual needs, a kind of labour hoarding that now gives employers more room to grow production cost effectively than the broader economic data imply.

- US Employment Data

The US economy added 428,000 new jobs in April, above the consensus forecast of 380,000.

The US employment backdrop is much different from the one in Canada, in part because the US Federal government’s emergency stimulus programs did not prioritize keeping employees tied to their employers.

The impacts of that different approach are borne out in the data. While the US GDP is now well above its pre-pandemic level and recovered much faster than in Canada, the US employment and participation rates still haven’t fully recovered (as a reminder, the participation rate measures the number of adults who are either working or are actively looking for work).

Somewhat strangely, after several months of robust recovery, the US participation rate dropped by 0.2% in April, which works out to 363,000 Americans withdrawing from the workforce. That is despite the fact the number of job openings increased by 205,000 and now stands at more than 11 million (or about two job vacancies for every unemployed American).

Average US wages rose by 5.5% in April on a year-over-year basis but slowed from 0.5% in March to 0.3% on a month-over-month basis. US inflation is now 8.5%, so the average American’s purchasing power is shrinking. That gap will form a powerful headwind for demand and will do some of the work that would otherwise be left to Fed rate hikes.

- Recession Odds

It now appears increasingly likely that both the US and Canadian economies are headed for recession.

US GDP growth was negative 1.4% in the first quarter on an annualized basis, and Fed Chair Powell acknowledged last week that the Fed’s goal of attaining a soft landing for the US economy will be “challenging”. Eleven out of the Fed’s last fourteen rate-hike cycles have been followed by a US recession and the pace of tightening this time will likely be more rapid and severe than most of those previous cycles.

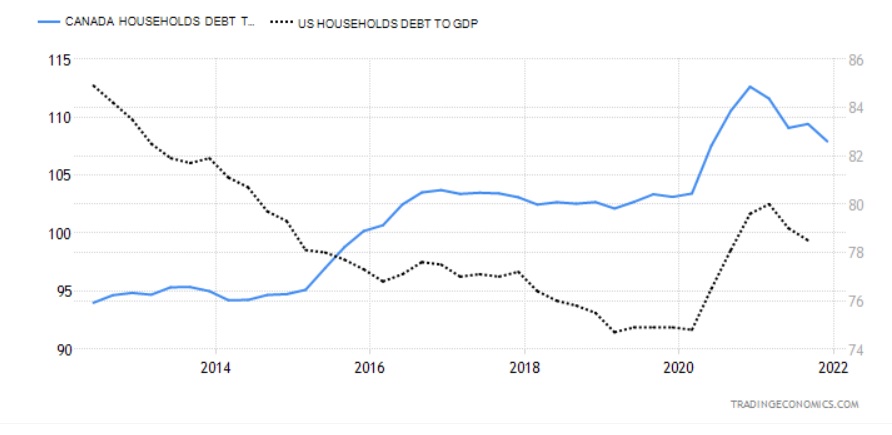

The Canadian economy is starting from a better place. Our GDP grew by 5.6% in the first quarter on an annualized basis. But our household debt-to-GDP ratio is high at 108% compared to 70% in the US. The higher Canadian debt level means that the relative impact of BoC rate hikes will be magnified (see chart).

Also, our economy is much more dependent on the interest-rate-sensitive real-estate sector, which accounts for 10% of our GDP versus 6.2% in the US, so any slowdown in that area will likely be more profoundly felt in the Great White North.

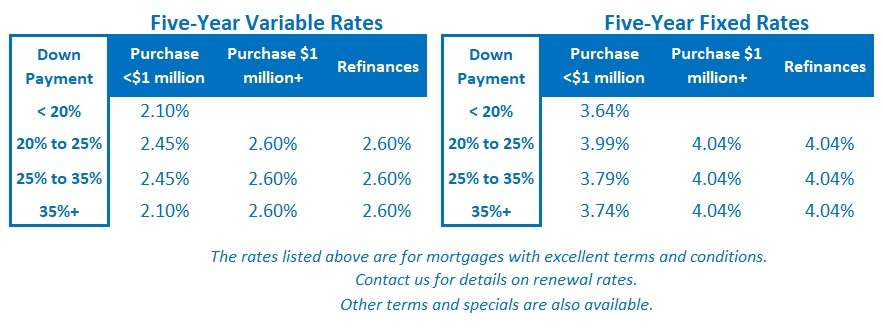

- Implications for Canadian Mortgage Rates

Fixed mortgage rates keep rising, increasing the temptation to grab one before they move higher. But that also heightens the risk that borrowers who choose a fixed rate will be locking in at a peak. The more sharply rates rise, the greater the likelihood that they will drop materially on the other side of the cycle.

Given that likelihood, the most important feature in any fixed-rate mortgage today is the penalty cost to break it, because over the long run, there is a good chance that a small difference in the rates will pale in comparison to a large difference in breakage costs (which you can learn more about here). Flexibility is key in today’s volatile market.

Variable mortgage rates continue to offer a compelling discount when compared to their fixed-rate equivalents, but that gap is expected to close rapidly in the months ahead. The bet for any variable-rate borrower today is that inflation will fall more rapidly then expected, and/or that a hard economic landing will force the BoC and the Fed to slow their pace of monetary-policy tightening (which includes both rate hikes and quantitative tightening).

For my part, and I recognize that this is a minority view, I continue to believe that five-year variable rates are more likely to save money when compared to five-year fixed rates over their full terms. But I must confess that I cannot offer that assessment with as much confidence these days. Realistically, anyone opting for a variable rate should expect it to rise by a minimum of 1% to 1.5% over the next 12 months and is well advised to increase their monthly payments today in preparation for that outcome. (It is the prospect of rate reductions before the end of the five-year term that still makes the variable-rate option compelling.)

The Bottom Line: The Government of Canada (GoC) five-year bond yield rose another 0.19% last week to its highest level in more than a decade. There was a short-lived bond-market sell off, which caused yields to fall after last week’s Fed announcement, which I actually predicted in last week’s post. But it didn’t last long. For the time being, the momentum for bond yields and fixed mortgage rates is still pointed straight up.

Variable mortgage rates remain well below their fixed-rate equivalents, but borrowers should not be lured by that gap because it will shrink rapidly in the months ahead. Variable-rate discounts off lender prime rates have also been shrinking of late, but they appear to have stabilized for the time being.