Our New Canadian Mortgage Landscape?

April 13, 2020Canadian Mortgage Rates Are Finally Starting to Fall

April 27, 2020 The Bank of Canada (BoC) held its policy rate at 0.25% last week, as was universally expected.

The Bank of Canada (BoC) held its policy rate at 0.25% last week, as was universally expected.

The Bank also released its latest Monetary Policy Report (MPR) but without its usual economic forecasts for foreign and domestic economic growth over the next three years. The BoC assessed the outlook as “too uncertain at this point” and decided that “it would be false precision to offer its usual specific forecast.”

No argument here.

The Bank did speculate that relative to the fourth quarter of 2019, our GDP dropped between 1% and 3% in the first quarter and will likely drop between 15% and 30% in the second quarter. On a related note, last week Statistics Canada confirmed that our GDP dropped by 9% in March, marking our steepest monthly decline since record keeping began in 1961.

Here are five highlights from the BoC’s latest policy statement and accompanying MPR, followed by my take on the implications for our fixed and variable mortgage rates.

- Our economy is being hit with a double shock – The BoC assessed that our economy’s “significant and rapid contraction” is primarily a result of “measures that authorities are implementing to control the spread of the virus” but that “the plunge in the global price of oil, is also weighing significantly on the Canadian economy.” The Bank noted that the price of a barrel of Western Canadian Select (WCS) is now “close to 90 percent lower than in January.”

- The BoC is pulling out all the stops – At his last emergency rate cut meeting BoC Governor Poloz said: “A firefighter has never been criticized for using too much water.” Thus far the Bank has purchased approximately $200 billion in assets, which works out to about 10% of our GDP. Then last week it announced that it will purchase up to another $50 billion of our provincial government debt and $10 billion in corporate bonds (while also extending the terms on short-term repurchase (repo) agreements out to 24 months). The Bank has now enacted thirty-four new policy measures since March 4 in an attempt to lower borrowing costs and keep our credit markets from seizing up. That’s a lot of water.

- Inflation is getting harder to measure – The BoC observed that crisis conditions make accurately forecasting inflation more difficult because its models use a fixed weighting for each price category that does not “capture changes to consumer spending patterns.” For example, today changes in food prices (which are rising) are more significant than changes in travel costs (which are falling). The Bank’s inflation models don’t adjust for the fact that one is impacting wallets a lot more than the other right now.

- The BoC is more worried about below-target inflation than above-target inflation – The Bank acknowledged that “the balance of forces points to weaker demand and a decline in inflation as the dominant concern.” In its best-case scenario, “inflation would increase gradually as the effects of past oil-price declines dissipate, the economy strengthens and excess supply is absorbed.” In its worst case, “a slower, more protracted recovery … [leads] to prolonged weakness in inflation through persistent excess supply.” If the Bank’s most likely outcomes for inflation fall between a gradual recovery and prolonged weakness, then …

- The BoC’s next rate change is likely a long way off – The Bank reiterated that its policy rate is now at its “effective lower bound”, which, simply put, means the bottom of its range, and that it is there to “lay the foundation for the post-containment economic recovery.” If it won’t go any lower, and it isn’t headed higher until our recovery is clearly evident, then our policy rate isn’t likely to go anywhere for some time.

Against that backdrop, you might be wondering why our mortgage rates aren’t lower.

The BoC has tried to reduce borrowing costs but thus far, the credit markets haven’t cooperated. The Bank’s rate cuts have been met with higher risk premiums that have increased funding costs, and at the same time, lenders have become (understandably) more cautious with their pricing.

Our policy makers have initiated other steps to help as well, such as providing massive amounts of liquidity, lowering capital requirements for lenders, and purchasing mortgages that were being held on lender balance sheets.

This powerful combination of measures may finally be working.

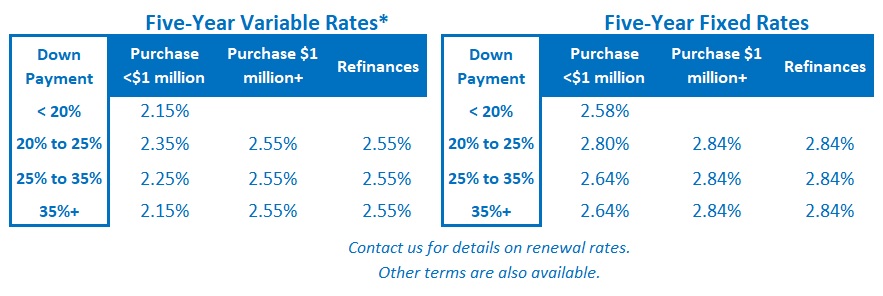

Fixed mortgage rates inched down late last week. As is their wont, lenders take the elevator when they raise rates and prefer the stairs when they lower them. Nonetheless, the BoC will take this is an encouraging sign that rates are at least moving in the right direction.

I want to close this week with an acknowledgement.

Last weekend I provided Globe and Mail personal finance columnist Rob Carrick with some estimates of the cost to defer mortgage interest for an article that he published on Monday. There were errors in my calculations and the information I provided was inaccurate and has since been corrected.

I would like to apologize to anyone who read the incorrect information I provided, and especially to Rob Carrick, who has supported my blogging efforts for years. I need to do better and I will.

The Bottom Line: The BoC held its policy rate steady last week and decided against providing forecasts in our highly uncertain environment. The Bank announced still more programs that were designed to keep our credit markets flowing and confirmed that below-target inflation is its “dominant concern.”

Fixed and variable mortgage rates fell a little late last week and that’s an encouraging sign that some stabilization may be setting in. Time will tell.