How Savvy Canadians Are Saving Thousands on Their Mortgages

October 28, 2019Should Canadian Variable-Rate Borrowers Lock in Now?

November 11, 2019 The Bank of Canada (BoC) held its policy rate steady at 1.75% last week, as expected.

The Bank of Canada (BoC) held its policy rate steady at 1.75% last week, as expected.

That means variable mortgage rates, which move in direct response to BoC policy-rate changes, will remain at their current levels for the time being. But the Bank’s increasingly cautious assessment of our economic landscape and focus on downside risks have the consensus now predicting that it will likely cut in the near future.

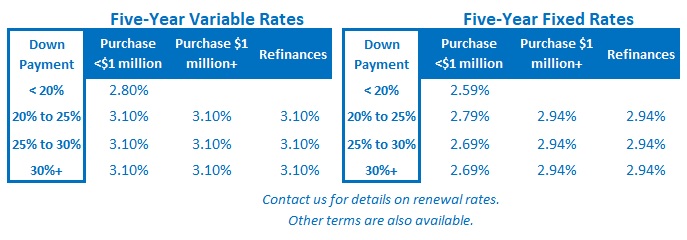

The BoC’s more dovish tone had an immediate impact on bond yields, and by association, our fixed mortgage rates.

The five-year Government of Canada (GoC) bond yield, which our five-year fixed mortgage rates are priced on, dropped by 0.15% shortly after the Bank’s latest announcement. If the GoC bond yield falls much farther, five-year fixed rates should move lower (subject to the old saw about lenders taking the elevator when they raise rates and the stairs when they lower them).

Here is a summary of my take on the BoC’s latest statement and its accompanying Monetary Policy Report (MPR), which is the Bank’s quarterly assessment of economic conditions both at home and abroad.

- The BoC started by acknowledging the trade-conflict elephant in the room, noting that its increasingly negative impacts have caused global economic momentum to slow to its weakest pace since the global financial crisis of 2007-09 and that “Canada has not been immune to these developments.” The negative impacts have been “most pronounced in business investment and the manufacturing sector” and have “contributed to a further deterioration in growth prospects and a fall in commodity prices.” The Bank estimates that in isolation, ongoing trade conflicts will reduce global GDP by 1.3% by the end of 2021, which is 0.5% higher than it estimated in its July MPR. Accordingly, it reduced its estimates for global GDP growth from 3.0% to 2.9% in 2019 and from 3.2% to 3.1% in 2020.

- The BoC noted that more than 35 central banks have cuts rates over the past three months “in reaction to weakening growth prospects and soft inflation expectations”, and financial markets “are expecting further monetary policy easing in the coming months.” Bluntly put, against that backdrop, it’s hard to imagine the BoC holding off for much longer.

- The Bank noted that U.S. bond yields have moved lower as investors seek safe-haven assets. Canadian bond yields closely track the movements of their U.S. counterparts and as such, the fall in U.S. bond yields has helped push Canadian mortgage rates lower without the BoC having to cut its policy rate (as Manulife Chief Economist Francis Donald noted in this recent BNN Bloomberg interview). The BoC’s decision not to cut has come at some cost. The Bank acknowledged that “the Canadian dollar has traded in a narrow range against the U.S. dollar while appreciating against other major currencies.” The relatively stronger Loonie is an intensifying headwind for our exporters, even more so after the U.S. Federal Reserve cut its policy rate by another 0.25% last week.

- The BoC now expects our GDP growth “to slow in the second half of this year”, largely as a result of “trade conflicts, continuing adjustment in the energy sector, and the unwinding of temporary factors that boosted growth in the second quarter.”

- The Bank had long predicted that our economy would transition away from consumer spending as its main growth engine and pivot instead toward business investment and export sales. But at his accompanying press conference, BoC Governor Poloz flatly acknowledged that this rotation has not occurred, and the Bank now predicts that both business investment and export sales will contract in 2019, before returning to modest growth in 2020 and 2021. The BoC now believes that our economic momentum will be underpinned by “a healthy labour market” and “solid income growth”, which will allow consumer spending to “increase at a steady pace”, even though the Bank also assessed its current trajectory as “choppy”, and it also expects housing activity to “continue its ongoing recovery.”

- BoC Governor Poloz noted the Bank’s concern that a rate cut could fuel a return to bidding wars in some regional housing markets. That said, he also noted that macroprudential policy changes like the mortgage stress test will help mitigate this risk, although he wasn’t entirely clear to what degree. Governor Poloz noted that the mortgage rule changes have led to a significant reduction in the number of stretched borrowers, which the Bank defines as anyone borrowing a mortgage that is more than 450% of their gross income.

- In the past the BoC has predicted that our output gap, which measures the gap between our actual output and our maximum potential output, would soon close. Interestingly, in its latest MPR it now only expects our output gap to “narrow” over the projected horizon, suggesting that the Bank now sees less inflationary pressure for our economy than in its previous forecasts.

- During the accompanying press conference, BoC Deputy Governor Wilkins observed that low rates magnify the impact of fiscal-policy stimulus. It has become somewhat of a tradition for the BoC to remind the federal government that fiscal stimulus would help to lighten their load.

- The BoC increased its forecast for our GDP growth in 2019 from 1.3% to 1.5%, largely on the strength of our surprisingly strong second quarter. It lowered its subsequent forecasts from 1.9% to 1.7% in 2020, and from 2.0% to 1.8% in 2021 and acknowledged that our economy will be “increasingly tested as trade conflicts and uncertainty persist.”

So what does all of this mean for our mortgage rates going forward?

The BoC has long talked about its need to anticipate the road ahead, and its latest MPR and accompanying policy statement make clear that it is increasingly concerned about downside risks both in the current environment and in the years ahead. That outlook portends lower rates on the horizon.

Against that backdrop, if you’re in the market for a five-year fixed-rate mortgage, it seems reasonable to believe that rates will move lower in the years to come. If that happens, borrowers who can find mortgages that allow them to break their contracts at reasonable cost will be able to take advantage of those lower rates (as I outlined in last week’s post).

Today’s five-year variable rates are still higher than their fixed-rate equivalents and that’s why the vast majority of borrowers continue to shun them. But economist David Rosenberg, who has an impressive track record with forecasting, made a powerful point last week that is worth considering. He wrote: “… historical statistical relationships would indicate that to offset the drag from the sharply weaker pace of global economic activity on Canadian GDP would imply nine rate cuts (so all the way to zero) or a move to, or through, C$1.40 for the Loonie (or some combination thereof.)”

Put simply, if past is prologue, Rosenberg predicts that variable mortgage rates could be headed much lower.

New borrowers through the door will probably still opt for cheaper fixed-rate alternatives, but that quote should give some comfort to existing variable-rate borrowers particularly those who have variable-rate mortgages with major banks and are wary of converting to their fixed rates, which come with prohibitively high penalties. The Bottom Line: The BoC held its policy rate steady last week but its more dovish outlook suggests that at least one cut may be on the near horizon. In the meantime, the Bank’s cautious language has helped to push GoC bond yields lower, and if this recent downward movement holds, the fixed mortgage rates that are priced on those yields should fall as well.

The Bottom Line: The BoC held its policy rate steady last week but its more dovish outlook suggests that at least one cut may be on the near horizon. In the meantime, the Bank’s cautious language has helped to push GoC bond yields lower, and if this recent downward movement holds, the fixed mortgage rates that are priced on those yields should fall as well.