Update On the Bank of Canada’s Latest Commentary with Implications for Canadian Mortgage Rates

December 19, 2011Happy New Year!

January 9, 2012 When the calendar flips to a new year, many of us make resolutions to improve our lives.

When the calendar flips to a new year, many of us make resolutions to improve our lives.

Judging by how busy the gyms get during the first three weeks of January, I’d bet that improving physical fitness is the most popular resolution, but improving one’s financial fitness is probably not far behind.

To that end, today’s post will offer you a simple mortgage tip to help you lower your interest cost, pay off your mortgage more quickly, and prepare for higher rates at renewal.

Canadian mortgage rates are at record-low levels and there has never been a better time to accelerate your principal repayment. The trick is to increase your regular payments by a relatively small amount to chip away at your principal over time, instead of waiting until you have saved up a chunk of money for a large extra payment (which for most of us tends to be a plan whose time never actually comes).

Most lenders will let you schedule an ongoing, automatic extra payment to be taken each time your regular mortgage payment is made, allowing you to ‘set it and forget it’. My advice is to calculate what your mortgage payment would be if your interest rate was 5%, subtract the amount you are currently paying, and use the difference as your extra payment.

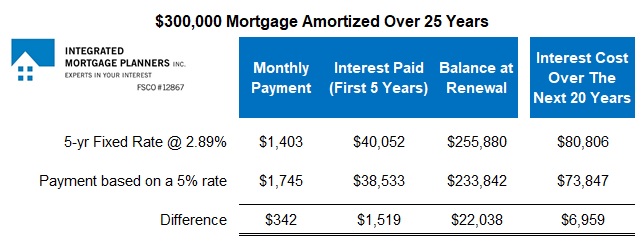

Here is an example of how this technique would work if your current mortgage rate was 2.89%:

Monthly payment for a $300,000 mortgage at 2.89% (25 yr. am) = $1,403

Monthly payment for a $300,000 mortgage at 3.29% (25 yr. am) = $1,745

Difference = $342

Now, take a look at what paying an extra $342 per month will achieve over time, and remember that the table below only assumes that you make the extra payment for the first five years (after that, it assumes that you revert to making the minimum payment at an interest rate of 2.89% over the remaining 20 years of your amortization period).

The additional $342/month adds up to $20,520 in extra payments over your fiveyear term and that will save you $1,519 in interest over the same period. More importantly, it will knock off an extra $22,038 of principal by the time your mortgage comes up for renewal.

That said, the real bang for your extra payment buck accrues over the longer term, because even if you go back to making your minimum payments after the first five years, you will still save another $6,959 over the remaining 20 years of your amortization period (bringing your total interest-cost saving to $8,478). That’s 42 cents in interest cost saved for each $1 of extra payment made, even with rates at record-low levels.

Basing your mortgage payment on a 5% interest rate will also significantly reduce your risk of payment shock if rates are higher at renewal – both because you will be used to paying a higher rate than the actual one in your mortgage contract, and because you will be renewing a lower balance at the end of your five-year term.

Bumping your monthly payment up to 5% is high enough to make a difference to your bottom line borrowing costs while still being manageable for most budgets. (To see what your mortgage payment would be at a 5% interest rate, check my mortgage calculator.)

Bumping your monthly payment up to 5% is high enough to make a difference to your bottom line borrowing costs while still being manageable for most budgets. (To see what your mortgage payment would be at a 5% interest rate, check my mortgage calculator.)

If you’re looking to improve your financial fitness in 2020, my advice is to turn the magic of 5% loose on your mortgage balance, and to steer clear of the gyms until early February when there are always plenty of workout machines to go around.