Monday Morning Mortgage Rate Update

June 30, 2025

Monday Morning Mortgage Rate Update – Canadian Fixed Mortgage Rates Are Increasing

July 14, 2025

Quick Summary: The US economy added more jobs than expected in June. That job strength will bolster US Federal Reserve Chair Jerome Powell’s plan to be patient with more rate cuts.

Quick Summary: The US economy added more jobs than expected in June. That job strength will bolster US Federal Reserve Chair Jerome Powell’s plan to be patient with more rate cuts.

Meanwhile, the Big Beautiful US budget bill passed. The consensus view is that it will stoke more inflation.

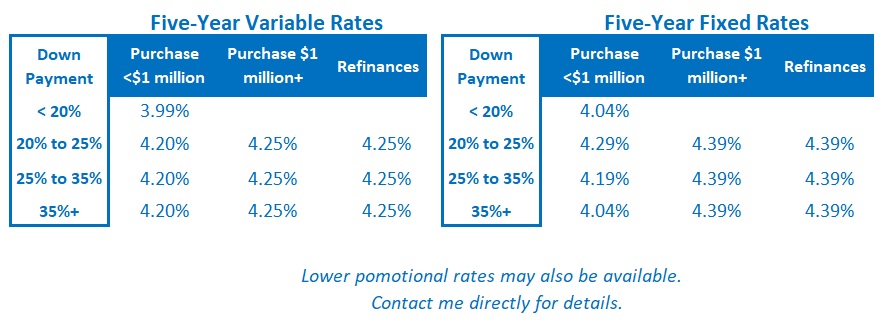

Mortgage Advice for Now

My advice is unchanged from last week.

Fixed rates remain below their long-term averages, and the rate premium that borrowers have historically had to pay for longer terms is slowly being restored.

For now, today’s best available three- and five-year fixed rates are roughly equal. For as long as that remains the case, I think five-year fixed rates offer better value.

I continue to believe that today’s variable mortgage rates will likely produce the lowest borrowing cost over their full term. But these are volatile times. Anyone choosing a variable rate should do so only if they can live with its inherent potential for volatility and if they have the financial capacity to withstand higher costs (and, in some cases, payments) should my forecast prove incorrect.

If you are interested in a more detailed explanation of the rationale behind my current mortgage-selection advice, check out this post.  The Bottom Line

The Bottom Line

Government of Canada (GoC) bond yields were pulled higher last week by their rising US equivalents.

Bond-market investors expect aggressive fiscal spending to stoke US inflation pressure. While the impact on prices from tariffs has been muted thus far, they are also expected to add inflation pressure.

Interestingly, last week Fed Chair Powell said the Fed would have already cut its policy rate by now if it weren’t for the tariffs. No word yet on what he thinks of the passage of President Trump’s expansionary spending bill.

While GoC bond yields, and the fixed mortgage rates that are priced on them, still appear range bound, a breakout higher seems more likely than a move lower at this time.

The Bank of Canada now has more justification to cut over the near term. Our latest inflation data showed early signs that our inflation pressures have started to ease after their recent uptick.

If that trend continues, it will increase the Bank’s flexibility to cut its policy rate to help offset the slow and steady deterioration of our economic data (GDP, employment, retail sales).

I still believe that a stimulative policy rate will ultimately be needed, but it won’t be considered stimulative until it is reduced to at least 2.00%. (Reminder that the BoC’s policy rate currently stands at 2.75%.)

Three Posts I Think Every New Visitor to My Blog Should Read

This post provides a detailed comparison of the pros and cons of fixed- and variable-rate mortgages.

This post provides a detailed breakdown of the different ways that lenders calculate their fixed-rate mortgage penalties. The amounts charged can vary significantly. A lower penalty can save borrowers thousands of dollars if rates drop.

This post provides a detailed summary of the key terms and conditions to pay attention to in your mortgage contract.