How Will the Iran War Impact Canadian Mortgage Rates?

March 9, 2026

Last week Statistics Canada confirmed that our economy shed 84,000 jobs in February, well below the consensus forecast that 10,000 new jobs would be added.

Last week Statistics Canada confirmed that our economy shed 84,000 jobs in February, well below the consensus forecast that 10,000 new jobs would be added.

The losses were spread across both our goods-producing (-28,000) and service-based (-56,000) sectors and concentrated in the private sector, which shed 73,000 jobs.

Our unemployment rate increased from 6.5% in January to 6.7% in February, and our labour force participation rate (which measures the percentage of working-age Canadians who are either working or actively seeking employment) also declined by 0.1%.

The heady job creation our economy enjoyed in the closing months of 2025 is now a distant memory. Two consecutive months of job losses to start 2026 (our economy shed 25,000 in January) have now essentially reversed all those gains. In other words, our economy hasn’t added any net new jobs over the last six months.

When we last heard from the Bank of Canada (BoC), it said that it would continue to hold its policy rate steady while it awaited an accumulation of evidence to confirm that its baseline forecast needed recalibrating.

Since then, our GDP data have failed to clear the low bar set by the Bank, our inflation data have cooled by more than expected, and our latest employment data now signal a worrisome turn in our labour market.

At this point it isn’t entirely clear how much evidence the BoC will need to be convinced that our economic trajectory is materially deviating from its baseline forecast. But it is clear that those deviations have all been in the same direction. Lower.

My contrarian call that the BoC would enact additional rate cuts in response to weaker-than-expected economic data was looking prescient right up until the moment that the US/Iran war started.

Oil prices surged higher as the bombs fell.

Iran has now effectively blocked the Strait of Hormuz, through which about 20% of the world’s oil moves, and oil production infrastructure in Iran, Saudi Arabia and the UAE has now been attacked and/or damaged.

Oil prices aren’t likely to normalize before the conflict cools, but there is no end in sight for that.

The BoC can’t ignore spiking oil prices. They have a pervasive impact on costs throughout our economy – both directly, on energy prices, and indirectly, as an input cost to produce plastics and move other goods.

For now, the threat of oil-price induced inflation should roughly offset the BoC’s concerns about the deflationary impacts from weakening overall demand.

I expect the Bank to highlight both upside and downside inflation risks in its policy statement this week and to hold its policy rate steady while it waits to see how these competing tensions bear out.

The Latest on Mortgage Rates

Government of Canada (GoC) bond yields continued their upward march last week.

They were pulled higher by a combination of rising US Treasury yields and spiking oil prices. That was despite Stats Can confirming our worst month for job losses (outside the pandemic period) since 2009.

Lenders continued to increase the fixed rates that are priced on GoC bond yields in response.

The typical fixed rate has increased by about 0.20% thus far. But GoC bond yields have increased by about twice that, so there is potential for additional near-term fixed rate increases from here.

Variable-rate discounts have remained unchanged thus far.

Surging bond yields will raise borrowing costs and cool demand in ways that are similar to monetary-policy tightening. In other words, the higher that bond yields rise in response to spiking oil prices, the less urgency there will be for BoC rate hikes.

All told, the BoC is almost certain to hold its policy rate steady this week.

My Take on Today’s Mortgage Options

Fixed rates are on the rise. Anyone who is actively looking to purchase within the next 120 days should lock in a pre-approval rate now.

Three- and five-year fixed rates remain the most popular choices. For as long as the spread between these two options is minimal, I think five-year fixed rates offer better value.

I continue to expect variable mortgage rates to produce the lowest borrowing cost over their full terms, although I have less confidence in that view than I did before the start of the US/Iran war.

The BoC will likely look through the oil-price spike over the near term. But if the war drags on and the inflationary impact from higher oil prices becomes more pronounced, there will come a time when the Bank must tighten. For now, my best guess (and hope) is that we won’t get to that point.

Important note: Anyone choosing a variable rate should do so only if they are comfortable with its inherent potential for volatility. Borrowers must also have the financial capacity to withstand higher costs (and in some cases, higher payments).

Insider’s Tip for Borrowers

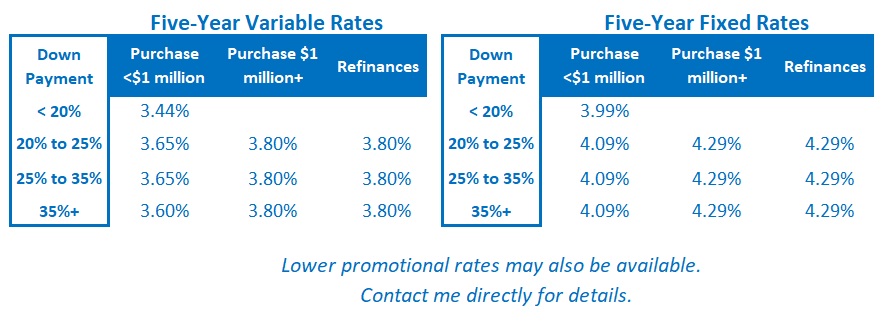

Did you know that borrowers who put down less than 20% of the purchase price of a property get the best rates?

If that doesn’t makes sense to you, it will after you read this post.

Three Posts Every New Visitor to My Blog Should Read

This post provides a detailed comparison of the pros and cons of fixed- and variable-rate mortgages amidst trade-related economic uncertainty.

For myriad reasons, some of them unanticipated, many Canadians end up having to break their fixed-rate mortgages. This post provides a detailed breakdown of the very different ways that lenders calculate their fixed-rate mortgage penalties. The amounts charged can vary significantly from lender to lender.

This post provides a detailed summary of the key terms and conditions to pay attention to in your mortgage contract. (They are not standard and can vary in important ways.)