Monday Morning Mortgage Rate Update – The Bank of Canada’s Next Move?

July 28, 2025

Monday Morning Interest Rate Update – How Job Losses Are Impacting our Mortgage Rates

August 11, 2025

Highlights From Last Week

Highlights From Last Week

The Bank of Canada (BoC) held its policy rate steady last week, as expected.

The Bank decided, once again, not to provide its usual economic forecast because “US trade actions remain unpredictable”. Instead, it presented different tariff scenarios that could play out.

The key takeaway was that the BoC sounded willing to enact more rate cuts if needed (and if inflation allows). Overall, this was a dovish hold.

The US Federal Reserve also held its policy rate steady last week, but unlike the BoC, the Fed’s accompanying commentary was more hawkish than expected.

Fed Chair Powell cited the “solid” US labor market, the persistence of above-target inflation, and the fact that there was still “a long way to go” before the full impact of tariffs becomes clear.

Despite his comments, US bond market investors now have the odds of a rate cut at the Fed’s next meeting on September 17 at 95%.

Those odds spiked higher on Friday after the release of the latest US employment data.

It confirmed that the US economy added only 77,000 new jobs in July, lower than expected. But more importantly, the previous employment estimates for May and June were revised lower by 258,000 jobs. That marked the biggest revision in a non-COVID month going back to 1979.

Here is some more context on this hot topic of conversation.

Revisions to initial payroll estimates are common. Because the US employment data are difficult to track in real time, the non-farm payroll data include many statistical plugs that are based on historical trends.

In stable conditions, those plugs help to smooth out short-term anomalies that ultimately prove to be just “noise”. But at turning points in the economic cycle, those plugs muffle the employment data’s power to signal when a material change is occurring.

Over time, however, revisions are made, and the signal becomes clearer.

In this most recent case, the signal is that the US labour market, and by extension, the US economy, may not have as much momentum as previously believed.

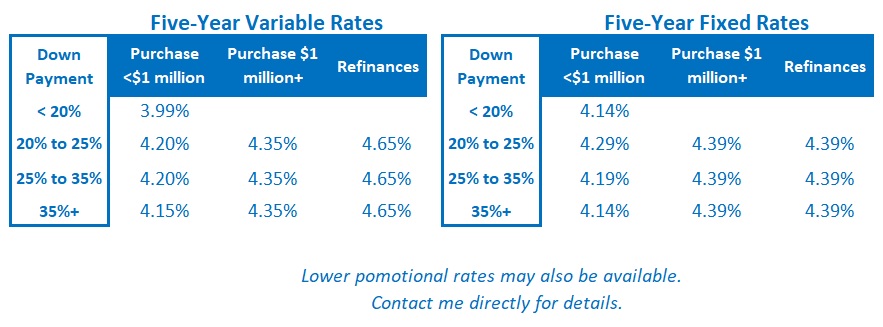

The Latest on Mortgage Rates

US Treasury yields broke lower on Friday in response to the latest US employment data. Their decline took our Government of Canada (GoC) bond yields along for the ride.

If GoC bond yields hold at Friday’s lower levels, that will put downward pressure on our fixed mortgage rates at a time when many lenders were in the process of raising them.

The near-term path for our fixed rates should be clearer by the end of this week, when the bond-market’s still-unfolding reaction has had more time to play out.

The BoC’s dovish tilt in its latest policy statement should give variable-rate borrowers hope that more rate cuts are on the way (and I continue to believe that will happen). But the bond-futures market is only pricing in about a 15% chance of a cut at the Bank’s next meeting on September 17.

In the meantime, the variable-rate discounts offered to uninsured mortgage borrowers have narrowed of late, which means that the variable rates offered to this subset of borrowers are now a little higher.

Insider’s Tip for Borrowers

Closing costs can be a nasty surprise for buyers who haven’t planned for them.

This calculator will help you estimate them, and this blog post provides a detailed explanation of each closing-cost category.

Mortgage Selection Advice

Fixed rates are now near their long-term averages. The term premium, which is the additional cost that borrowers must pay to lock in for longer terms, is slowly being restored as our bond-yield curve continues to normalize.

Right now, the best available three- and five-year fixed rates are roughly equal. As long as that remains the case, I think five-year fixed rates offer better value.

I continue to believe that today’s variable mortgage rates will likely produce the lowest borrowing cost over their full term, even now that additional BoC rate cuts are taking longer than expected.

Anyone choosing a variable rate should do so only if they can live with its inherent potential for volatility. Borrowers must also have the financial capacity to withstand higher costs (and, in some cases, higher payments) should my forecast prove incorrect.

Three Posts I Think Every New Visitor to My Blog Should Read

This post provides a detailed comparison of the pros and cons of fixed- and variable-rate mortgages.

This post provides a detailed breakdown of the very different ways that lenders calculate their fixed-rate mortgage penalties. The amounts charged can vary significantly from lender to lender. A lower penalty can save borrowers thousands of dollars if rates drop.

This post provides a detailed summary of the key terms and conditions to pay attention to in your mortgage contract.