Last Week’s Glimpse Beyond the US/Iran War

April 20, 2026

The Bank of Canada Holds Steady (and Offers Some Reassurance)

May 4, 2026

The Bank of Canada (BoC) will almost certainly hold its policy rate steady when it meets this week.

The Bank of Canada (BoC) will almost certainly hold its policy rate steady when it meets this week.

It doesn’t yet know whether the global energy-price spike will be sustained for long enough to stoke inflation pressure across our broader economy. But there is not much evidence of an inflation pass through from higher energy prices thus far.

Last week Statistics Canada confirmed that our Consumer Price Index (CPI) increased from 2.2% in February to 2.4% in March, which was below the consensus forecast of 2.6%.

The Bank’s preferred measures for core inflation, CPI-Trim and CPI-median, were little changed. They came in it at 2.3% and 2.2% respectively on an annualized basis and have been running well below 2% when measured across the most recent three months.

While higher energy prices will likely push our CPI higher in the months ahead, other disinflationary factors will help offset their impact.

Slowing economic growth has increased the amount of slack in our economy overall. Consumers and businesses are more pessimistic and are spending relatively less. Tighter credit conditions are weighing on demand. Shelter costs, which had been the primary cause of our above-target inflation in the post-COVID years, are now exerting downward pressure on our CPI.

Higher energy costs also keep demand in check. They act like a tax on the rest of our economy, because consumers and businesses can’t substitute away from them. More money spent on energy leaves less to spend in other areas of our economy.

Put me down for a rate hold by the BoC this Wednesday and for dovish accompanying policy-rate language that should put to rest speculation that the Bank will be hiking any time soon.

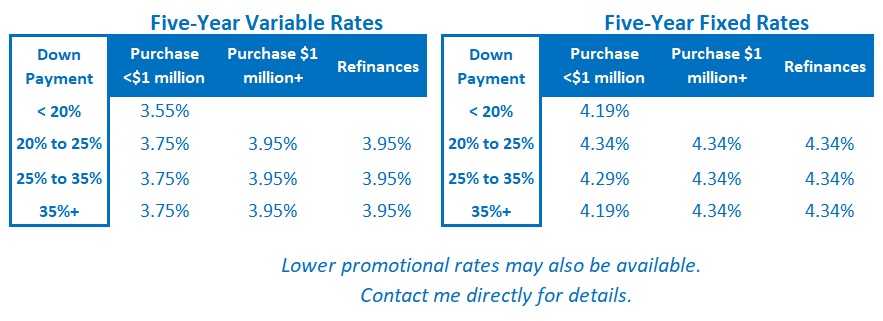

The Latest on Mortgage Rates

Government of Canada (GoC) bond yields remained range bound last week.

Fixed mortgage rates held steady, but borrowers should be prepared for more volatility ahead.

Variable-rate discounts were also unchanged.

Bond-market investors are no longer pricing in BoC rate hikes in 2026, after previously pricing in three imminent 0.25% increases at the outset of the US/Iran war.

I expect the BoC to remain on hold for the time being. But I still expect the Bank’s next move, when it eventually occurs, to be a cut. That assessment is based, in part, on the assumption that the factors contributing to disinflation in our economy will outlast the US/Iran war’s inflationary impacts.

My Take on Today’s Mortgage Options

My advice is unchanged from last week. Fixed rates are likely to remain volatile.

Three- and five-year fixed rates remain the most popular choices. If the spread between those two options is minimal, I think five-year fixed rates offer better value.

Most of the borrowers I am working with right now are opting for the stability of fixed rates, and I fully appreciate their appeal.

That said, the relative saving offered by today’s variable rates has increased now that spiking bond yields are putting significant near-term pressure on fixed mortgage rates.

I expect that variable mortgage rates will produce the lowest borrowing cost over their full five-year terms, although the potential that they will take borrowers on a bumpy ride has increased since the start of the US/Iran war.

BoC Governor Macklem has confirmed that the Bank will look through the oil-price spike over the near term. But if the war drags on and the inflationary impact from higher oil prices becomes broader and more entrenched, there will come a time when the Bank must tighten.

For now, my assessment is that we won’t get to that point. But so much depends on how long the US/Iran war will last and if/when the Strait of Hormuz will re-open. That remains an open question.

Important note: Anyone choosing a variable rate should do so only if they are comfortable with its inherent potential for volatility. Borrowers must also have the financial capacity to withstand higher costs (and in some cases, higher payments).

Insider’s Tip for Borrowers

This post offers mortgage advice to homeowners who are trying to work through a divorce.

It outlines some key steps that must be taken prior to removing a spouse from title and/or completing a refinancing to buy them out. It also includes several other useful tips that I have accumulated over many years of helping borrowers navigate a marital split.

Three Posts Every New Visitor to My Blog Should Read

This post provides a detailed comparison of the pros and cons of fixed- and variable-rate mortgages amidst trade-related economic uncertainty.

For myriad reasons, some of them unanticipated, many Canadians end up having to break their fixed-rate mortgages. This post provides a detailed breakdown of the very different ways that lenders calculate their fixed-rate mortgage penalties. The amounts charged can vary significantly from lender to lender.

This post provides a detailed summary of the key terms and conditions to pay attention to in your mortgage contract. (They are not standard and can vary in important ways.)